Dedicated Geological Storage of CO2 Set to Dominate CCUS

Author: Eve Pope, Technology Analyst at IDTechEx

Carbon capture, utilization, and storage (CCUS) technologies remove carbon dioxide (CO₂) from flue gases or directly from the atmosphere, before either storing this captured carbon dioxide underground or using it for a range of industrial applications. CCUS has been identified as one of many vital decarbonization technologies that will be needed to meet global net-zero emissions targets. The new IDTechEx report “Carbon Capture, Utilization, and Storage (CCUS) Markets 2025-2045: Technologies, Market Forecasts, and Players” covers all aspects and technologies of the CCUS value chain.

Recently, a subtle change in language has emerged at conferences and expos in the CCUS space. IDTechEx analysts have noticed that policymakers and key industrial players have solely focused on carbon dioxide storage more and more. CCS (carbon capture and storage) has taken centre stage, increasingly dropping the “U” (utilization) from discussions.

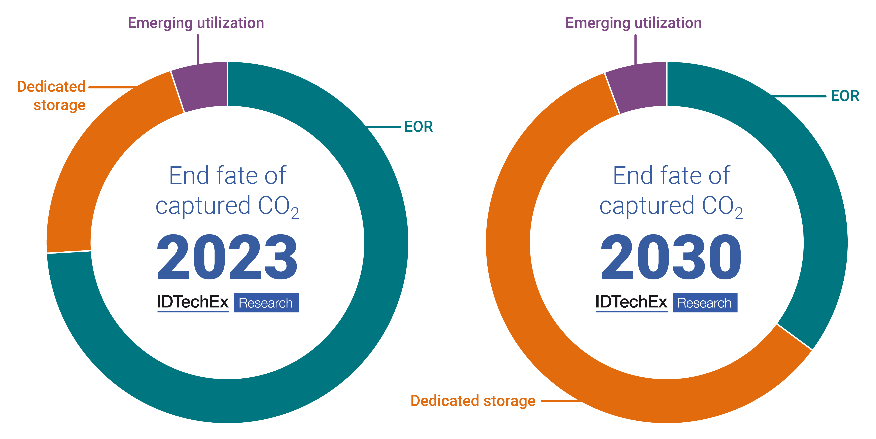

About 75% of existing CCUS projects rely on utilization of CO2 to achieve profitability via enhanced oil recovery (EOR), a method of reversing productivity decline in oil fields while storing CO2 underground. According to IDTechEx forecasts, dedicated geological storage of carbon dioxide will outpace EOR as the leading end fate of capture CO2 by the end of the decade. By 2045, IDTechEx forecasts the world will be sequestering 1.6 gigatonnes per annum of CO2 underground. Key reasons for this paradigm shift in CCUS are explored in this article.

IDTechEx forecasts that dedicated geological storage will outstrip EOR as the leading end fate of captured carbon dioxide by 2030. Source: IDTechEx

There is now a business model for dedicated CO2 storage

When carbon dioxide is permanently sequestered underground, most commonly in saline aquifers, no tangible product is created. However, the global rise in carbon markets and carbon pricing mechanisms has provided a business model for storing CO2. Carbon pricing provides an economic method of addressing climate change: a cost is applied to greenhouse gas emissions to encourage polluters to reduce their carbon footprints. The EU ETS (emission trading system) is a prime example. When government carbon pricing instruments result in emitting CO2 being more expensive than capturing, transporting, and sequestering CO2, CCUS can thrive.

The last decade has seen carbon pricing expand to more sectors in more regions, with prices generally being higher now than ever before. Other financial government incentives for CCUS have also emerged, such as the US 45Q tax credit. This increased economic driving force for CCUS has stimulated project development, with several large-scale CO2 storage projects are in the pipeline. Major oil and gas players such as Shell, Equinor, and Chevron are leveraging decades of subsurface expertise to open-up storage in saline aquifers.

Permanently storing CO2 is better for reaching climate targets

Permanently storing carbon dioxide generally has better sustainability credentials than utilizing CO2. This is because permanently sequestering CO2 captured from an industrial process in dedicated underground storage is a net-zero process (or even net-negative for some CO2 sources). In contrast, captured CO2 returns to the atmosphere on short time scales for several CO2 utilization applications, such as when a fuel synthesised from CO2 is combusted. Storing CO2 is therefore better suited to meeting emission reduction targets.

Furthermore, there is simply greater potential for CO2 storage than CO2 utilization. It is estimated that the world’s potential CO2 storage capacity may exceed 15,000 gigatonnes. To put this into perspective, global anthropogenic CO2 emissions are currently around 40 gigatonnes per year. This far outsizes potential utilization markets for carbon dioxide, even when including emerging application areas such as CO2-derived chemicals or CO2-derived concrete products.

Where will CO2 utilization still shine?

Fossil fuel infrastructure won’t disappear overnight, but existing assets can be decarbonized. New CCUS enhanced oil recovery projects are still expected in the future because the oil produced by this method has a much lower carbon footprint than typical oil extraction. Alternatively, drop-in replacements to fossil fuels can be made by utilizing CO2, such as CO2-derived e-fuels. Such low-carbon fuels are seeing demand from the aviation and maritime sectors, where full electrification remains unfeasible for decarbonization.

For carbon dioxide utilization applications that permanently store CO2, such as carbonate formation in CO2-derived concrete, similar regulatory support to dedicated geological storage may be available. For example, utilisation in such a way that CO2 becomes permanently chemically bound (or mineralised) is considered the same as underground geological storage under the EU ETS, while also generating a product that can be sold to generate revenue (such as a concrete aggregate or additive).

Finally, CO2 utilization can act as a transitionary fate of CO2 because the necessary CO2 transportation/storage infrastructure to support large-scale CCUS does not yet exist for most regions. Many such CO2 storage projects plan to be operational before 2030, with the Northern Lights Longship project expected before the end of 2024, but some emitters will remain without access. In the short term, CO2 utilization could allow mature ready-now carbon capture technologies to be deployed as infrastructure expands.

For more information on CCUS, please refer to the IDTechEx “Carbon Capture, Utilization, and Storage (CCUS) Markets 2025-2045: Technologies, Market Forecasts, and Players” report.

For more information on CO2 utilization, please refer to the IDTechEx “Carbon Dioxide Utilization 2025-2045: Technologies, Market Forecasts, and Players” report.